Systemic Banks, Capital Adequacy and the Case for Credit Suisse

17 March 2023

Capital Adequacy

Under Basel III (international regulatory framework for banks), the minimum capital adequacy ratio which banks are required to maintain stands at 8%. (The capital adequacy ratio measures a bank’s capital in relation to its risk-weighted assets).

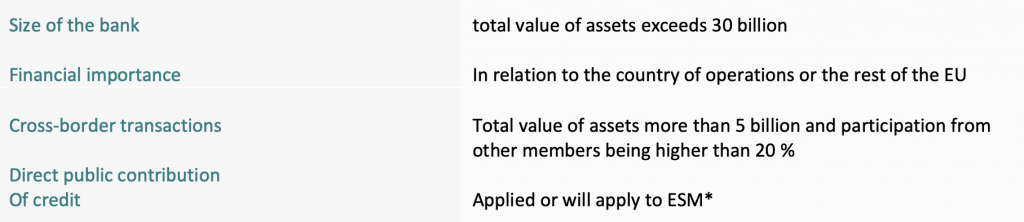

The definition of a systemic bank is the following:

“A systemically important financial institution (SIFI) is a bank, an insurance company, or any other financial institution whose failure might trigger a financial crisis.”

They are colloquially referred to as “too big to fail”, however there are certain criteria to classify a bank as being systemic.

Therefore, the two parameters which ones needs to consider when conducting banking forecasting are the following:

- the sustainability of the bank to survive;

- the means which the bank has in order to survive (what were their interest charges in the last few years) and whether a bank focuses only on specific investment schemes, for example the Silicon Valley Bank (SVB) which focuses on Technology Funding, Technological Start-ups, and Technology investments.

Some introductory facts about the Silicon Valley Bank (SVB)

On the SVB webpage, the bank: “Announced commitment to provide $5 billion in sustainable finance and set goal to achieve carbon neutral operations by 2025” and

“Welcomed Kay Matthews as Chair of SVB Board of Directors”:

It has been previously stated that banking and finance are heavily influenced by the trending e.g. global goals for “Green development” alongside with technology projects/startups/ environmental issues are always fashionable and trendy. The result would be that as a bank they focus mainly on Startup banking; Venture Funding & Corporate Banking, and from their 2022 results we understand that they adhered indeed to the above-mentioned activities:

Financial Highlights for 2022

- $212B assets

- $74 B total loans

- $342B total clients’ funds

It can be then stated that Credit Suisse is indeed systemic, and yet the recent loan from the Central Bank of Switzerland put on alert investors; money makers; private equity holders and the markets in general.

As per multiple news sources across the globe: “An assistance of 50 billion Swiss Francs was granted to Credit Suisse from the Swiss Central Bank – something which has never before been recorded, while the bank’s shares fell in a race below even 30 % of their value, and at the closing price stood at -24.24%.

The decision of the regulator of Switzerland’s stock exchange (FINMA) and the Swiss Central Bank to “support” Credit Suisse is considered to be absolutely vital, otherwise the repercussions of letting Credit Suisse go bankrupt, would have been impossible to contain and far reaching.

The academia on the matter and world-renowned economists reject the 2008 scenario and aim and hope for a sustainable future.

A new European stress test with regards to basic interest rates will be the main point of discussion in the months to follow, across EU territory. Raising it will contribute to inflation, however keeping it ‘frozen’ or at a stand-still, will slow-down financial progress. The stability of the nexus of the basic interest in comparison to the dropping of inflation is the major goal, to maintain sustainable economies in the Eurozone and the rest of the globe. Therefore it was decided to raise the basic interest rates in order to match the cost of rising inflation. Some Greek scholars commented that Europe becomes a ‘target’ and this decision also exploits vulnerability of Central Banks to manage crises. We have to follow-up the Financial Agenda to eventually make remarks on current affairs.

It looks like the systemic banks which affect the rest of the economy with their performance, cannot decide blindly or in vain, and technocratic members of the Board of Directors know exactly how not to spread panic in the global markets. Otherwise, we will have learned nothing from the well-known story of Lehman Brothers.

And unfortunately, the unexpected collapse of the Silicon Valley Bank – even though its figures showed fantastic performance – was an example that lack of trust in the performance of a bank and fear of liquidity commands transferring of big amounts in addition to making problem seem larger than it really was.

The eventual decision to secure only $250 K for each SVB account owner, looks like a big hole in a system that is repeatedly agile and never recovers either via mechanisms or otherwise.

* European Stability Mechanism

For best practices on banking & finance and for professional advice on which legislation applies in the Republic of Cyprus, please contact us directly at agp@agplaw.com

The information provided by A.G. Paphitis & Co. LLC is for general informational purposes only and should not be construed as professional or formal legal advice. You should not act or refrain from acting based on any information provided above without obtaining legal or other professional advice.